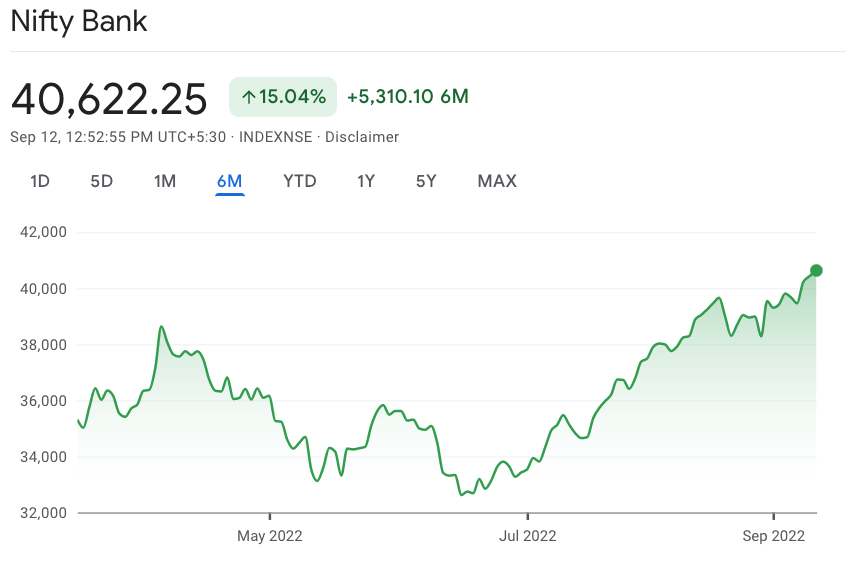

Bank Stocks have given spectacular returns over the last 3 months. Nifty Bank has rallied by nearly 24% since it bottomed out just 3 months ago in June 2022.

Source : Google

Not only in absolute terms but also relatively, Nifty Bank outperformed broader market indices such as Nifty 50, Nifty next 50 and Nifty 500, by a margin of 6-10% over the last 6 months.

Source : Google Finance

That’s all well and fair but what are the key factors behind this rally?

We believe the following factors have contributed to this movement.

- The Theory of Mean reversion is a theory in finance that states that asset prices and/or asset volatilities will revert i.e – come back to its long term mean (average). Put simply, any asset that has undergone significant movement in prices over and above (or below) its fundamentals should revert back towards prices that are justified by its long term fundamentals i.e – some sort of mean.

The last 5-7 years have been especially painful for the banking industry.

NPAs rose sharply between 2015 – 2018, credit growth slowed down and corporate debt, which makes up a large chunk of the overall loans in the system, either had to be restructured or paid down on a priority basis.

Then the IL & FS crisis happened in late 2018 and then Covid-19 in March 2020.

Because of the above factors and many others that cannot be exactly pinpointed, the banking sector performed poorly in terms of share prices, profitability and credit growth.

The NPA problem has slowly been correcting itself as large corporates paid down their debt and NPAs reduced, leading to sharp increases in profitability and a some sort of reversion to the mean (after a long period below the so called ‘mean’)

- Because a Banking industry is cyclical in nature, peak cycle profitability is correlated to increasing credit growth rate.

And Over the last few quarters, credit growth has consistently inched higher and higher reaching ~15% (y-o-y) as of the end of August 2022.

Source : livemint.com

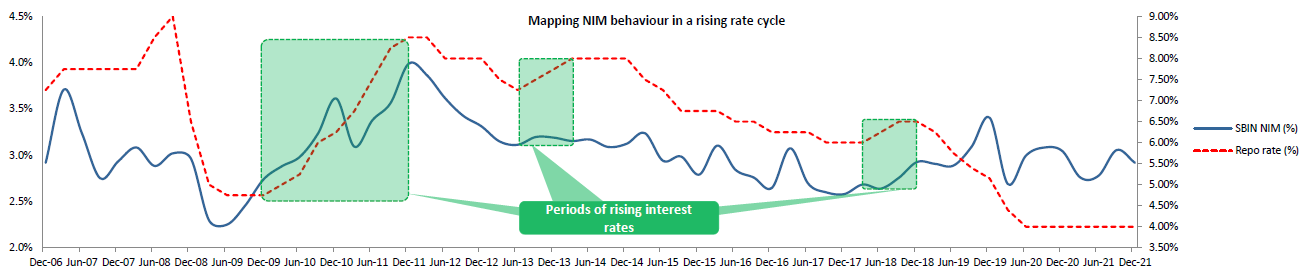

- Rising interest rates increase the cost of borrowing for the banks itself and eventually for customers.

On a first thought, it would seem that increasing interest rates should impact credit growth because the cost of borrowings goes up, however, in the short run a positive correlation has been observed between increasing interest rates and credit growth, even historically.

The simple reason is that Net Interest Margin, which equals Interest Earned – Interest paid, expands.

NIMs expand with increasing interest rates because banks are able to reprice (pass on) the increase in interest charges on loans much more quickly than they are willing/able (in some cases) to pass on the increase to the depositor in the form of Interest paid.

Therefore, temporarily, an increase in interest rates leads to an expansion in NIMs, which are a proxy for Sales for a bank.

And when sales increases, keeping other costs largely stable, most banks expect an increased profitability in the short run.

Infact, here’s an interesting graph that shows this phenomenon (shaded green) for SBI historically. Where rising interest rates lead to NIMs expanding.

Source : www.livemint.com

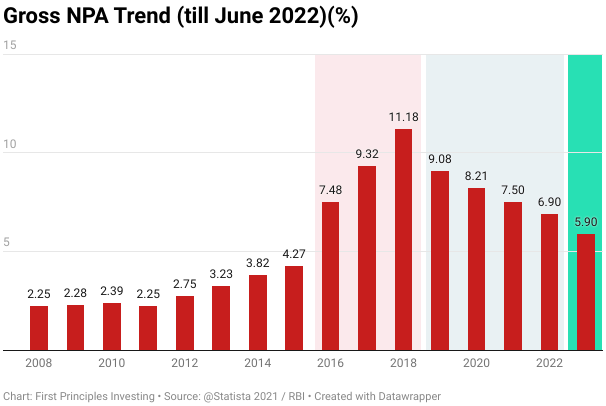

3. Low NPA Cycle

As we discussed earlier, the Indian bankings’ bad loans nightmare is mostly behind us.

And there has been a steady decline over the last few years, with GNPAs reaching a low of 5.9% as of June 2022.

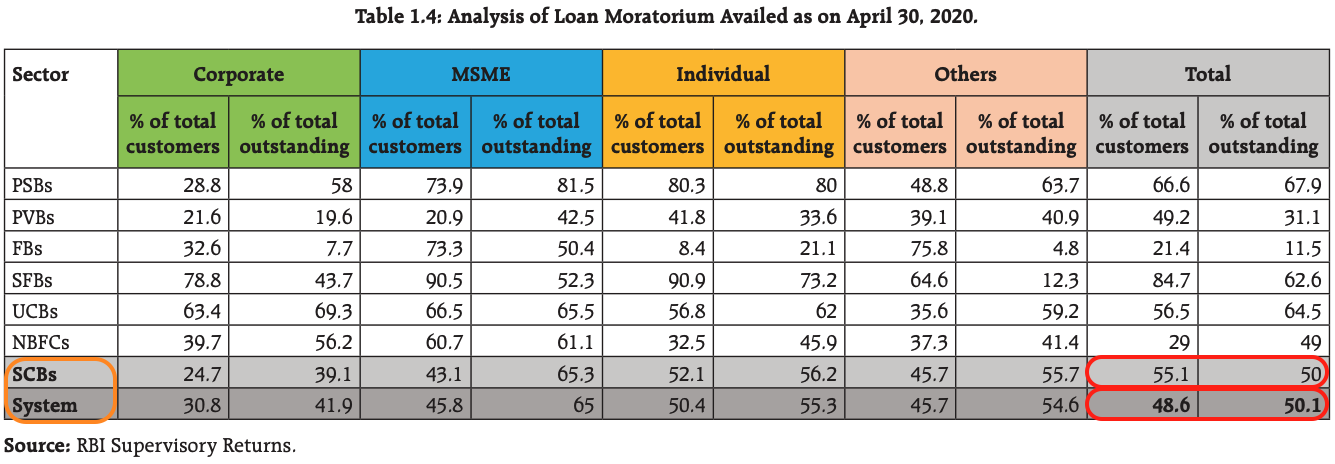

This is an obvious surprise for the entire industry because when the covid lockdown happened Banks were likely going to be one of the worst hit.

The initial data suggested things could get really bad.

For example, nearly 50% of all loans were under moratorium as of April 2020

According to the Financial Stability Report for the period ending June 2020, The RBI was expecting that the GNPA ratio of Banks may increase from 8.5 per cent in March 2020 to 12.5 per cent by March 2021 under the baseline scenario; and may escalate to 14.7 per cent under a very severely stressed scenario.

So, it was a pleasant surprise when the GNPA ratio declined steadily over the last few quarters instead of rising to 14.7% as was initially projected under the ‘severe stress scenario’.

Which leads us to the next point

4. FII Interest : Unexpected positive surprises lead to re-ratings and re-ratings lead to investors’ interest and investor interest leads to a lot of money chasing the same sector/stocks, which leads to sharp increase in prices.

FII allocation to BFSI sector declined to 34.2% in the Nifty 500 as of March 2022, a multi quarter low

And while data is yet to be confirmed for the September quarter, it is obvious that FII demand has led to a sharp uptick in Bank Nifty

So, is the sharp rally in the bank nifty sustainable ? Is it supported by fundamentals?

I can’t comment on the sustainability of the rally but it is true that Earnings data clearly shows that the banking sector is in an upcycle.

Bank Nifty EPS (earnings per share) has quadrupled since 2020.

This quadrupling of EPS is a direct result of sharp decline in NPA, because higher NPAs require higher provisioning expenses which reduce profit.

So, much of the increase in EPS over the last 2 years has happened because of NPA reduction.

For the upcycle to sustain for longer, whether for next few quarters or maybe years, most of the profit growth can only come from credit growth i.e loan book growth.

The NPA reduction lever for profit increase has largely been exhausted and credit growth is the key factor that will likely result in increasing profitability.

Which brings us to a key risk, which is that Interest rates are rising because of higher than desired inflation in the economy.

While in the short run, rising interest rates result in NIM expansion and likely profitability, this is unlikely to be sustainable because at one point the higher rates will act as a detriment for borrowing further, slowing down the credit growth.

So, how the dynamics between interest rates & inflation play out will to a large extent determine credit growth and thus, the sustainability of the upcycle in the banking sector.

So, should you invest today in the Banking sector ?

There are 2 ways to take a bet on the banking sector, either by investing in Bank Nifty, a proxy for the banking sector or individually into select stocks.

We will leave out individual stocks because that would require more in depth analysis on a case by case basis but if we were to potentially invest in the banking sector as a whole, we could possibly think like this :

Since Bank Nifty is an Index, investing in a Bank Nifty ETF will provide more diversification and lower volatility versus if we were to invest in individual bank stocks.

But how do you know whether Bank Nifty is overvalued, undervalued or fairly valued?

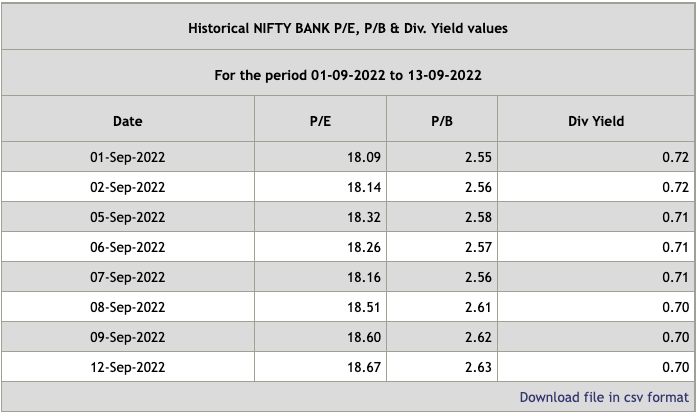

We need 2 sets of Data, PE Ratio & EPS growth of Bank Nifty.

Next we compare the current PE Ratio with Bank Nifty’s historical average, which is ~ 18, taken as an average of the lowest and highest value observed from 2003 till date.

So, PE Ratio of Bank Nifty is effectively at its ‘fair value’

Next, we combine PE Ratio with EPS growth, which as we discussed is in an upcycle.

So, essentially, we can think like this : An Investor is able to buy a basket of Bank Stocks at a PE of 18 (approx. its average value) with the added optionality of :

- Higher than Normal Credit Growth

- Higher than normal EPS Growth

It may be a reasonable buy.

Of Course, the ideal situation would’ve been if PE was below its average value and credit growth growth and EPS growth prospects were as they were.

Another thing to bear in mind is that there is the obvious risk that RBI may not be able to handle the inflation even with the already increased interest rates, warranting further rate hikes, which would dampen the demand for loans and thus credit growth and thus profit growth of the banking sector.

So, did you find this way of analyzing Bank Stocks interesting? Let me know in the comments section.

Disclaimer :

- I am NOT a SEBI Registered Investment Advisor, but then again, this is NOT investment advice. This post is best interpreted as Educational

- Despite my suggestions that Nifty Bank may be a reasonable purchase, along with the risks highlighted above, I personally have not invested in Bank Nifty in the 3 months prior or since writing the post.

2 thoughts on “Banking Sector in a game of Musical Chairs?”

Thanks for sharing your thoughts on the Indian Banking sector… very helpful!

You’re most Welcome Rohit sir. More articles coming soon.